I just started to wonder about the cost of Covid measures to our government and where all the money for this comes from. It is not a simple thing, and for someone like me I need it grossly over-simplifying if I am even to begin to understand. According to the BBC news, this year the government is spending £280 billion on measures to fight Covid-19 and its impact on the economy. If you want to see it as a number here it is:

280000000000

So where is it coming from? And the entire National Debt is currently £1,876.8 billion (at the end of the financial year ending 2020). So who has that sort of cash to lend the government?

If you want to see what this 1,876.8 billion looks like then here it is:

1876800000000

Whoever lent that money will collect 23.5 billion in interest.

The government borrows money by selling bonds. A bond is a promise to make payments to whoever holds it on certain dates. There is a large payment on the final date – in effect, the repayment. Interest is also paid to whoever owns the bond in the meantime. So it’s basically an interest-paying “IOU”. The buyers of these bonds, or “gilts”, are mainly financial institutions, like pension funds, investment funds, banks and insurance companies. Private savers also buy some.

Some also end up being bought by the Bank of England as part of its current attempts to boost spending and investment in the economy. Under this policy – known as “quantitative easing” – the Bank has so far bought £875 billion of government bonds.

Now all that seems a bit crazy to me because if you look on the Bank of England’s website it will tell you that they are “wholly-owned by the UK government”. The Bank was nationalised in 1946, which meant that it was now owned by the Government rather than by private stockholders. So the government borrows money by issuing bonds, which it then buys itself. So where does that money come from to buy its own bonds?

However, not all of the above is quite true, because 3% of the bank’s shares are owned by private investors. Just as when the bank was originally set up, the identities of these shareholders is a closely guarded secret. In fact, when, in 2009, a request was made to HM Treasury, under the Freedom of Information Act, asking for the details about the 3% Bank of England stock owned by unnamed shareholders, the response was that their identity was something the Bank was not at liberty to disclose. In a letter of reply dated 15 October 2009, HM Treasury explained that. “Some of the 3% Treasury stock which was used to compensate former owners of Bank stock has not been redeemed. However, interest is paid out twice a year…” But whoever that 3% are, will they be taking that percentage of the interest payments on the £875 billion, or £26250000000?

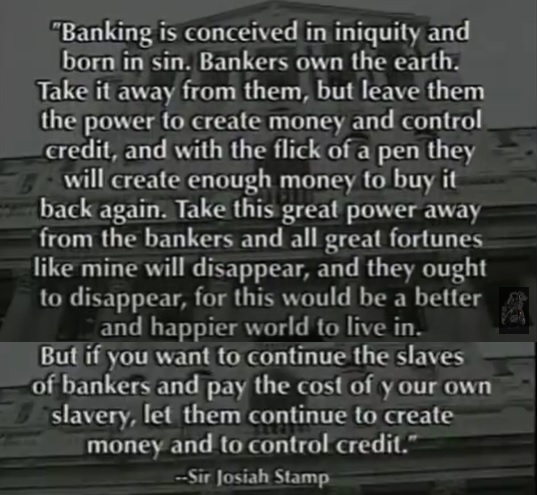

These sort of figures boggle the mind! So, I tried to find out more online. It turns out that most “national banks”, although they may give themselves names that sound like government departments, like “The First Bank of the United States”, are privately owned. Even the “nationalised” Bank of England is not wholly owned by the government. The history of these powerful institutions, who have the power to issue money, is complex. What is certain is that some people must have made silly amounts of money out of it.

It goes back to the notion of “fractional reserve banking”. Bankers realised that only a fraction of investors wanted to withdraw their money at any one time, so the idea came about that they could lend out more money than they actually had, making profit from the interest payments on loans. In fact, they were allowed to lend out up to ten times their reserves under fractional reserve banking rules. And royalty or governments were the ideal targets for large, profitable loans, underwritten by the power to tax the population. Fractional reserve banking meant that the banks didn’t actually have to have the cash in order to loan it.

So imagine that I am a National Bank. OK, I’m patently not, but just humour me for a moment. I have one pound, but under the laws of fractional reserve banking I can lend out £10 (don’t forget that I also have the right to create money from thin air by printing currency if I need to). But it is only numbers on a balance sheet, not actual cash when it comes down to it, which is transferred between accounts. From that loan I may get back, say £11 when interest is added. So now I can loan out £110… and so on. I wondered why the bankers don’t just print themselves all the money they want, but putting too much money out there would only increase demand for goods and services and lead to price inflation, which would devalue the currency. If I find that there is too much money out there and inflation is rampant, then I can constrict the money supply by calling in debts or not issuing new loans. In short, there is nothing “natural” about the cycles of boom and bust which our economies are subject to. They are entirely manufactured by those who control the money supply: in other words the National Banks.

So back to my original question: who has that sort of cash to loan the government? I think the answer is that that sort of cash simply does not exist. It’s all just numbers on balance sheets, but somewhere along the line someone, somewhere is likely to be making huge profits from this crisis. These people must love national crises like the pandemic, or wars, because huge profits can be made by loaning the money to pay for them to governments. Historically banks have actually financed both sides (for example during the Napoleonic Wars) with clauses that require the victors to honour the debts of the vanquished.

If you want the full story (and have some stamina – it’s three and a half hours long) give this a watch and it explains the whole sordid tale of how we have got to this stage:

I actually had to watch this twice to get my had around it. But now I think I need a lie down…

Absolutely amazing, Pete. Although I did have to laugh at the part where the government lends itself the money! I have been asking myself this question for a while. Thank you for some clarity. I say ‘some’ as I am still a simple Yorkshireman 😉

LikeLiked by 1 person

Yes Charlie, I too am a simple Yorkshireman by birth. Check out Bill Still to completely blow your mind!

LikeLike

For a minute I thought you’d written it yourself – not that you aren’t clever – but all that is very taxing on the brain. We’ve said all along, it’s just monopoly money and best ignored. (I always thought that about austerity and the National Debt) However Mike and I are in the fortunate position of being retired , so furlough, redundancy etc doesn’t really affect us.

LikeLiked by 1 person

Looking at this again, it seems that I was wrong – sorry, you did write it! I can’t delete my last comment, or I would! However, just to follow up on what I said – your explanation is fascinating, but confirms what I’ve always thought about the billions governments talk about – although, I suppose that if your country does go bankrupt, like Zimbabwe and others, my idea that it’s only monopoly money doesn’t hold true. I think I need to read your blog when I’m wide awake! 🙂

LikeLiked by 1 person

Anne, thanks for your thoughts. You banged me to rights with the paragraph that begins “The government borrow money by selling bonds…” which I “borrowed” from a BBC News site. But the rest is from this addled brain. You make a fascinating point about countries going “bankrupt”. I think that this must mean that other countries will no longer buy their government stock because they have defaulted on loans. With a country like Zimbabwe I would imagine that a lot of government bonds would have been purchased by their guilty former colonial master, who knew its potential as the “breadbasket of Africa”. There is still much I just don’t understand in all this.

LikeLike